The five I’s of Europe’s energy transition – from Power Summit Lights ON

Eurelectric’s Power Summit kicked off in Greece this year with an inspiring vision for the future of Europe’s energy transition, spelled in five key priorities – or I’s. Against the backdrop of the recent European elections, several key challenges lie ahead for the EU’s journey to net-zero: a cost-of-living crisis, aggressive foreign competition in clean energy technologies, deindustrialisation and energy security, among others. But there are a few success stories learned in the past five years that will help our Union navigate the next five years of the new legislative mandate.

The EU success stories

‘’We committed to making Europe the first continent to achieve climate neutrality by 2050’’ – recalled the European Commissioner for Energy, Kadri Simson,

at Power Summit, highlighting EU Member States’ strong, unified response to crises such as the COVID-19 pandemic and the energy crisis, which have further accelerated the energy transition.

“Gas storages are now already more than 60% full which is 24% higher than the previous historic average. Gas amount has been reduced by 19% over past year and a half, saving around 124 billion cubic metres of gas. Imports of Russian energy and pipeline gas have plummeted to 15% in 2023 compared to 45% in 2021.” – stated Simson.

The EU’s efforts have led to record increases in renewable energy capacity and significant strides in electrifying transport and buildings. However, the need for greater uniformity and unity among all Member States is evident to meet the ambitious targets set by the EU’s. Some member states, however, are leading by examples in their energy transition journey. Speaking of successful example, Greece, the hosting country of our Summit this year, was praised for his many achievements in its green transition and the remarkable status of the country’s energy sector today.

As declared by the Greek Prime Minister Kyriakos Mitsotakis:

“The country’s Public Power Corporation (PPC) was once Greece’s most pressing problem, lagging far behind. Today, it’s a different picture altogether – [PPC has become] a serious player on the European stage.’’

Such transformation highlights Greece’s broader energy transition path, one fuelled by significant investments in renewable energy and grid infrastructure.

Georgios Stassis, CEO of PPC, echoed this sentiment, initially focusing on Greece's advancements in renewable energy:

‘’Solar and wind capacity has doubled, over 60% of hydropower is generated by green technologies and Co2 emissions have dropped by 60% too”.

Stassis then emphasised the necessity for Europe to work together in delivering the transition and replicating similar outcomes across the Continent - "Unity is the magic word. When we work together, we achieve remarkable results," Stassis asserted.

What’s needed with the next Commission: the five I’s

From success stories from the past five years, a more sobering undercurrent pervaded the discussion when looking at Europe’s future. According to Kristian Ruby, Secretary General of Europe should focus on the famous three I’s: implementation, investments, and infrastructure.

To this crucial mix, two additional I’s were voiced during the Summit: innovation and industrial competitiveness. Both have emerged as indispensable tools to succeed with Europe’s climate and energy targets while keeping a thriving industrial base in Europe .

This was echoed by Commissioner Simson:

“Looking ahead we must continue to nurture Europe’s industrial competitiveness and clean tech manufacturing sector. At the same time we need to consolidate the strengths of our energy union to make sure it delivers on our 2030 climate and energy targets and we can prepare for 2040 an beyond.”

It’s no wonder these will likely be the key priorities for the EU next legislative mandate.

Industrial competitiveness

Amidst shifting geopolitics, Ruby cautioned:

"Joe Biden’s 100% import tax on Chinese electric cars and the new world order proposed by Putin and Xi Jinping have placed Europe in a precarious position."

He stressed the importance of maintaining momentum in the green energy race for both energy security and economic stability. Dimitri Papalexopoulos, Chairman of Titan Cement, clearly mirrored this urgency, calling for a balanced approach to climate goals, energy sufficiency, and competitiveness: "We need a strategy, a sense of urgency, and purpose.

Innovation

Greater competitiveness demands higher digitisation, especially in the energy sector where the race for clean technology dominance has become especially fierce. The hard truth is that Europe lags behind in the digital realm.

. "Europe has been losing ground to Asia and the US for the past two decades, and this trend has accelerated recently," – warned Papalexopoulos,

emphasising the importance of leveraging technology and innovation for global competitiveness. ‘In the tech world, we have lost the race, particularly for AI’ – he added. A sentiment shared by Stassis, who believes ‘now more than ever, Europe needs to prioritise technology’.

To spur innovation and competitiveness, a growth strategy powered by forward-looking investment mechanisms and de-risking tools is crucial.

Investments

The investment needs of our energy transition are daunting. Cheap capital is no longer as readily available as it was a few years ago and public coffers are under pressure given the COVID-19, energy and cost of living crises.

In the immediate and near future, Europe will need to significantly ramp up investments in defence, the green transition, and the digital sector all while upholding the ‘European’ social order. Papalexopoulos pointed out that – ‘if you put this all together, the numbers just don’t add up.’

With annual investment needs nearing 4% of EU GDP, or €660 billion a year, EU countries are grappling with a fundamental question: where will we find the money to finance the energy transition?

“The challenge is so vast that Europe needs to consider solutions beyond the confines of conventional approaches.” – writes Ruby in an article on Sustainable Views. – “The good news is that several no-regret options are available to help bridge the investment gap.”

These include:

- de-risking investment tools such as counter guarantees issued by governments or the EU to reduce the risk profile of power purchasing agreements (PPAs),

- anticipatory investments to future proof our energy infrastructure,

- capacity mechanisms to guarantee an attractive business case several years into the future for dispatchable assets – including storage, hydropower, nuclear etc.

EU regulatory steering proves crucial to attracting the necessary investments. This is particularly evident in the power sector, where long-term investments signals are critical for utilities to justify decade-long investments and to incentivise the establishment of new production lines in critical supply chains. Special attention was paid to the investment needs of the power distribution grid, the often forgotten giant of the energy transition.

Infrastructure

“Investing in our energy infrastructure is not just us being prudent; it can be a win-win scenario." – said Papalexopoulos.

Infrastructure was indeed the key theme of our Power Summit this year. Eurelectric’s latest Grids for Speed study showed that Europe should invest around €67 billion in our power distribution grid each year from 2025 to 2050, that is double what we currently invest.

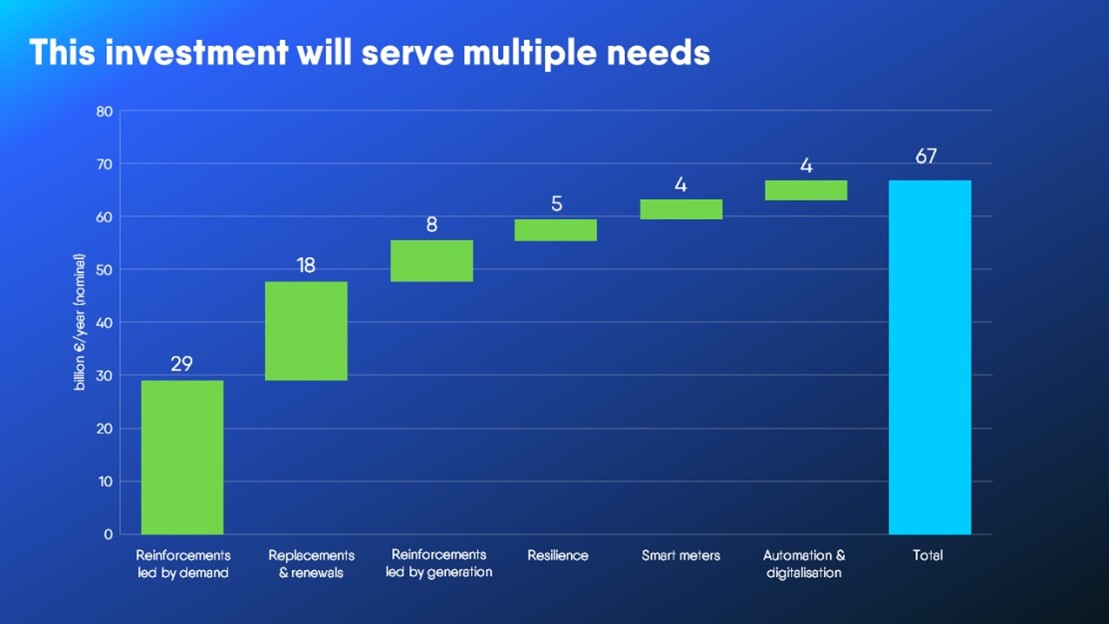

If we put numbers into perspective, however, this investment only corresponds to 20% of what the EU spent on fossil fuel imports in 2023. Getting the grid up to speed will significantly reduce fossil fuel imports, create more than 2 million jobs, bring greater energy savings and deliver more reliable power supply while accelerating the decarbonisation of Europe’s economy.

Notably, several grid trends and technologies could lower this figure to €55 billion per year if properly implemented. These include anticipatory investments, optimal asset management and grid-friendly flexibility. Failure to invest would jeopardise 74% of prospective connections in key decarbonisation technologies such as electric vehicles (EVs), heat pumps and renewables. Investing, on the contrary, will accelerate electrification and help the EU save €309 billion every year on fossil fuel imports from 2040 to 2050.

Implementation

Last but clearly not least, rather first, is implementation. Implementing the Green Deal is no easy endeavour. Andrea Gerini, Secretary General of NGVA Europe, underline:

"We are at the halfway point between the Paris Agreement and the 2030 deadline. Only 18% of companies are cutting fast enough to reach net zero by 2050. We need changes," Gerini stressed.

At present, progress is sluggish. The next Commission will thus need to streamline the execution of what has been agreed on in the previous mandates. As detailed in our Election Manifesto, newly elected policymakers should initiate appropriate assessment and adjustment rounds of implemented polices, rigorously monitor progress, and support Member States in meeting their targets while avoiding unnecessary changes of recently adopted energy legislation.

From success stories to future challenges, our Summit made one thing clear: a vision without resources is an illusion. And these resources can only be ensured if both industry and policy work together for a competitive, decarbonised and energy independent European Union.