The AI Race is on, but can we supply enough electricity to power it? – Power Summit 2024

There are three events that have completely changed Europe’s energy landscape in the past two years. The first, Russia’s tragic invasion of Ukraine (still ongoing). The second, the energy crisis that unfolded from Russia’s deliberate weaponisation of gas supplies, forcing Europe to rethink its energy security and lower its dependence on Russian fossil fuel imports. But there has also been a third revolutionary event with significant implications for the power sector.

It began in November 2022 in the US, and quickly arrived in Europe: ChatGPT.

Arshad Mansoor – President and CEO at EPRI – delves into how the subsequent technological boom intersects with the energy sector and its implications for the future at Eurelectric’s Power Summit 2024.

What does the AI race mean for the power sector?

Powering a “creative brain” like OpenAI takes a lot of energy. More than we can imagine. The success of this ground-breaking technology has led to an AI-driven surge in electricity demand which is expected to soar even higher in the coming years.

In Texas alone, electricity consumption is expected to match Germany’s entire usage within six years, driven by the rapid expansion of data centres for AI applications.

“They are adding Germany to Texas” – emphasises Mansoor.

Microsoft is looking to develop a 5GW AI data centre in collaboration with Open AI for $100 billion.

“That is one fourth the size of Greece [in terms of power demand]” - explains Mansoor.

Google is creating a $1.2 billion opening a data centre in Finland. Ana Paula Marques, Executive Board Member of EDP, captures the excitement perfectly - "We see a lot of hype on follow the money? More like follow the energy”.

‘We are on the cusp of a new steam engine era, with a massive increase in data centres.’ – notes Mansoor. “The impact of an artificial brain will be profound across every aspect of the economy and it will impact us”.

If not managed in a timely manner, however, this impact might be all but positive for electricity.

What’s happening to the supply?

The sector is already constrained on supply chain shortages, especially when it comes to power infrastructure. Meanwhile, our power grids are ageing in Europe and there are calls for a rapid modernisation and buildout of our transmission and distribution infrastructure. This means new substations, copper cables, transformers, switchgears and lots of red tape work to build out the power system of the future.

Current shortages of copper, a deficit of talent , extended manufacturing lead times and transformers’ costs all risk hampering infrastructure development and the needed electrification in Europe.

Eurelectric’s Grids for Speed study shows that transformer lead times have risen to 2.5 years on average in the last couple of years and up to 4 years for large transformers. As a result, copper is becoming scarce. Within the current decade, a shortfall in copper is anticipated. This risks triggering a price surge, frustrating the immediate acceleration in grid development unless the industry ramps up capacity quickly.

All of this begs the question, will Europe be able to power the AI race-is the supply there?

It can be if we address these bottlenecks through strategic planning, enhanced collaboration between European policymakers and industries as well as new training initiatives to streamline education certificates and ensure a skilled workforce. Policy support is also critical for securing an agile and resilient supply chain, from mineral extraction to procurement, for distribution grid development.

Meeting AI’s energy needs will not only require a dynamic mix of renewable sources and higher electrification, but also more advanced grid technologies that utilise the infrastructure already in place and insfrastructure that will be constructed in the future .

Grids up to speed

“10% to 15% of the grid is built to supply demand for 1% of the time, 87 hours in a year, we got to change that” – says Mansoor.

Several technologies can help optimise the grid such as dynamic line rating, smart transformers, smart meters, and the digital twin. Such technologies, together with forward-looking planning, can significantly lower the need for grid investments.

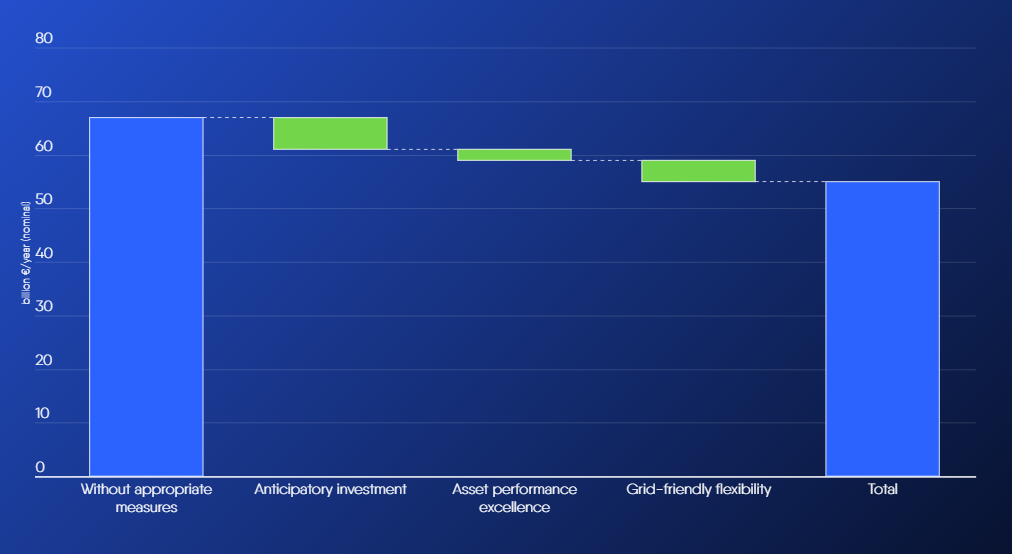

As shown in the above graph, grid investments could be lowered from €67 billion per year to €55 billion from 2025 to 2030 by enabling anticipatory investments, boosting grid-friendly flexibility and improving asset performance excellence.

The missing link, however, is a supportive regulatory framework. To change that, national regulators should allow distribution system operators (DSOs) to invest in an anticipatory manner to prepare our power infrastructure for massiveinscreases in electrification. This means removing barriers to anticipatory investments and incentivising DSOs with fair remuneration and a stable investment environment. Failure to do so would mean failing to power the EUs AI race and the decarbonisation of our economy.

As the conversation on AI drew to a close, one resounding message emerged at the Summit: integrating AI and its vast energy needs will be a critical driver of electricity demand. Europe must get ready for it.